The State of Supply Chain Tech

The supply chain is the backbone for any country. It is a huge industry, but is still archaic - even the basic principles of tech have hardly been applied yet. The supply chain in India is very inefficient. To benchmark with the US and China, the logistics costs (14% of GDP) in India is significantly higher than in China (9% of GDP) and the US (8% of GDP). The supply chain tech is still in its nascent stage. Only 1% of TAM is captured by supply chain tech companies. So, it is a huge opportunity for startups, especially in India.

Tech has been reinventing the supply chain and logistics industry. The supply chain tech is a very fragmented market, and there are many categories within this space:

SaaS offerings e.g. ERP, supply chain analytics and optimization, supply chain visibility software, etc.

Automation providers e.g. Warehouse automation players

Tech-enabled transactional services e.g. Freight, Fulfillment service providers, etc.

As tech tried to reinvent supply chains, I believe these companies have unbundled the supply chain/logistics industry and now they are rebundling it.

In this essay, I will particularly focus on tech-enabled transactional services companies and how tech has changed this category. The transactional providers have a high service component and transactional pricing. Tech is used to optimize labor-intensive internal processes and reduce costs. These companies also provide enhanced customer experience, real-time shipment visibility, and better service levels to their customers by leveraging technology.

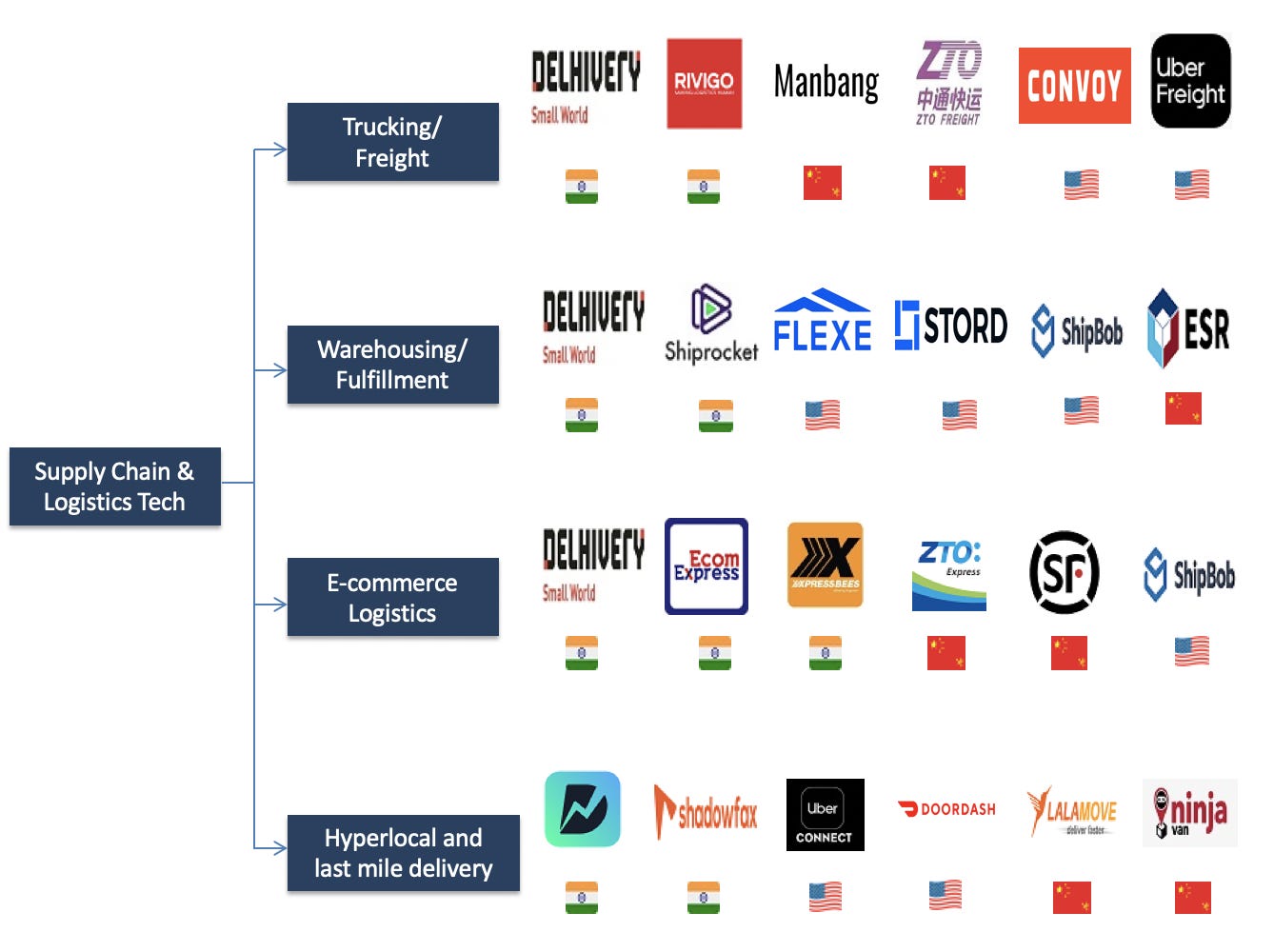

Tech-enabled Supply Chain Service Providers Landscape

To get a better sense of supply chain service providers, I mapped out the key players from India, US, and China in the major verticals. Please note that this is not an exhaustive list, the startups mentioned here are for illustration purposes.

Fulfillment

Companies in this category provide outsourced and on-demand warehousing and fulfillment services. As a part of warehousing, they conduct activities such as stock receiving, quality check, storage, pick, pack and ship. These startups provide multi-tenant and multi-location fulfillment centers, so clients can store inventory near the buyers without making any significant capital investment. Additionally, depending on the volume/seasonality, startups also provide on-demand storage. The players in this category provide omnichannel fulfillment. Various sales channels (e.g. retail, D2C, wholesale, etc.) are integrated and an order is sent to the WMS of the service provider. Depending on the order type (B2B, B2C), a courier is selected. Instead of using any off-the-shelf WMS, these companies have their own WMS platform, which allows them to provide better services. Startups like Stord and Flexe also operate a marketplace and connect warehouse providers with retailers and wholesalers for storage and fulfillment services.

E-commerce Logistics

The startups in this category provide logistics/shipping services to small, medium, and enterprise-level e-commerce and D2C companies. They provide the first mile (pick up a package from seller), middle mile (delivery to destination city via air/surface transportation), and last-mile (from last-mile hub to the customer’s doorstep) services. They offer pre-paid and cash-on-delivery payment options. Also, they provide same-day, next-day, 2-days and slot-based delivery services. Additionally, these companies also offer reverse logistics services and manage returns and replacements.

Freight/Trucking

This category involves startups that provide long haul and short haul freight services such as full-truckload, less-than truck-load and cold chain services. This vertical is fragmented and most of the companies in this category act as a marketplace - a middleman between a shipper and a carrier. Additionally, they also provide value-added services such as financial services, billing, etc.

Compared to incumbents, these startups provide real-time visibility in the shipment, high reliability and better pricing. Startups like Convoy have automated the load matching, which reduces their brokerage fees, and they match the load efficiently so that empty miles of carriers can be reduced. Some of the players in this category has SaaS-enabled marketplace. They have various tools built in such as billing, bidding, POD/BOL capturing, calculating accessorial charges, etc. to enable a transaction between a carrier and shipper.

Last Mile and Hyperlocal Delivery

Last-mile distribution is defined as the process of transportation of packages from a delivery center in the destination city to the customer’s doorstep. It is the last leg of the fulfillment process. There are startups that provide standalone last-mile services. Also, generally, the express package delivery service providers have last-mile capability.

As opposed to the last mile, Hyperlocal delivery refers to the process of delivering goods directly from a seller to the customer within an area in the same city. In this category, a delivery agent picks up products from a seller and then delivers them directly to the customer’s location. The deliveries are carried out in a small geographical area, and the deliveries are usually completed within a few hours (1-2 hrs). There are various types of startups in this category e.g. meal delivery, peer-to-peer delivery, goods delivery from a local store to a customer in the same city, etc.

Final thoughts

The above was a broad overview of supply chain and logistics tech landscape in terms of the supply chain services provided by tech startups. One thing that becomes clear is that while some companies have multiple services that target different services in the supply chain, there’s no one company that provides all of the services. These all startups started providing one of the services and have now expanded into other categories. So, we are witnessing rebundling of multiple services e.g. Delhivery started with express package services and then ventured into fulfillment, freight and E2E solutions services. This allows startups like Delhivery to cross-utilize assets and reduce the costs/improve the payback period of their CAPEX.

The startups that provide multiple services e.g. freight, fulfillment, express package delivery, etc. have also developed an integrated solution. For example, Delhivery and Stord have an integrated fulfillment + transportation platform that is used to conduct transactions, provide E2E supply chain visibility and optimize the supply chain.

Given these services providers have pretty thin margins, some of the companies might also start SaaS offerings in the future - the software (e.g. WMS and TMS) that is used internally to provide services can also be sold as SaaS to the retailers. Also, eCommerce companies like Flipkart and Amazon have their own logistics arms such as eKart and Amazon Transportation Services respectively, which is primarily used to support their internal logistics operations. But they might also start providing the 3PL services to other companies e.g. ATS has started providing freight services to shippers in the US.

It’d be interesting to see if new players will emerge or the moats of the existing players will be strong enough that it would make entry of new players difficult. In the subsequent essays, I look forward to digging deeper into each of the aforementioned categories (e.g. freight, fulfillment, etc.) within transactional services.

Disclaimer: I work at Delhivery.

Thanks for reading. If you enjoyed reading it, please share it with others. Also, if you have any feedback/thoughts, please tweet at me.